What Is A Bad Bank?

Editorial by Boyd Evan White

If you can’t get 100% of your money back from a Bank according to the terms you opened the account under, then, that is a bad bank.

In 2018, are there any bad Banks?

It has been a long time since the term a “Bank Run” has made the news; though there are occasional news items on Bank failures those usually don’t entail long lines of people trying to withdraw their money; moreover, that is because to a significant extent people do “get their money back”.

How is that? Because the Banks have acquired governmental insurance from the Federal Deposit Insurance Corporation (FDIC). The website ( https://www.fdic.gov ) gives the following information:

The FDIC is an independent agency created by the Congress to maintain stability and public confidence in the nation’s financial system by:

* Insuring deposits.

* Examining and supervising financial institutions for safety and soundness and consumer protection.

* Making large and complex financial institutions resolvable. and

* Managing receiverships.

Deposit insurance is a fundamental component of the FDIC’s role in maintaining stability and public confidence in the U.S. financial system. By promoting industry and consumer awareness of deposit insurance, the FDIC protects depositors at banks and savings associations of all sizes. When these IDIs fail, the FDIC ensures that the customers have timely access to their insured deposits and other services. The basic limit of federal deposit insurance coverage is currently $250,000 per depositor.

In the event of a Bank failure, the FDIC covers all the losses of the bad Bank. Prima facia, this sounds like a good thing so Bank customers do not get defrauded or stolen from; however, it also lessens the responsibility of Bank customers from learning the difference between a good and bad Bank and choosing to patronize good Banks. What business should the Federal government have in making good on the losses of bad Banks?

The Banking Crisis

The banking crisis of the 1980’s and 1990’s was the greatest challenge the FDIC had ever faced. The crisis had four main causes. Boom-and-bust economic activity occurred in certain regions and economic sectors. Legal restrictions on branching made banks more vulnerable to regional and sectoral recessions. Many banks exhibited weak risk management. And appropriate government policies, such as less-frequent bank examinations, also played a role.

These terms “weak risk management”, “appropriate government policies”, and “less-frequent bank examinations” are moot when a Bank is good and its customers have a strong contract for doing business with them.

The Federal Savings and Loan Insurance Corporation (FSLIC) was an institution that administered deposit insurance for savings and loan institutions in the United States. In the 1980s, during the savings and loan crisis, the FSLIC became insolvent. It was recapitalized with taxpayer money several times, with $15 billion in 1986 and $10.75 billion in 1987; however, by 1989 it was too insolvent to save. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA) abolished it and transferred the responsibility for savings and loan deposit insurance to the Federal Deposit Insurance Corporation (FDIC).

What shucking-n-jiving, how can a Federal institution go insolvent without the Federal government going insolvent. Are we to be painted as slack-jawed yokels who watch the name plates change and the hot potato juggled from one byzantine agency to another without demanding prosecutions?

How many times and to what extent has the FDIC had to cover the failures of Banks?

Looks like there have been lots of bad Banks. And the cost, in some years, runs into the billions of dollars. In how many of these Bank and Thrift failures were criminal charges filed?

That is a salient point concerning morality and ethics, if the FDIC covers all failures, with the source of that money being dubious (fiat and debt based), and there is no discernible punishment for criminality, then, there is no standard for badness, everything comes out good, and that smacks of Utopianism.

It is also interesting t o note from 1934 to 1979, about one half the life span of the FDIC, there were 558 Bank and Thrift failures, and from 1980 to 2017 there have been 2,065 Bank and Thrift failures. Quite a substantial increase in failure since 1979. And mind you, this is the era of a heavily inflated monetary system, there are trillions more dollars in circulation now than there were in 1979, everything should be supportive for having good Banks; but there is a substantial increase in failure. And the Utopian capability of the FDIC makes there seem like there are no bad Banks.

o note from 1934 to 1979, about one half the life span of the FDIC, there were 558 Bank and Thrift failures, and from 1980 to 2017 there have been 2,065 Bank and Thrift failures. Quite a substantial increase in failure since 1979. And mind you, this is the era of a heavily inflated monetary system, there are trillions more dollars in circulation now than there were in 1979, everything should be supportive for having good Banks; but there is a substantial increase in failure. And the Utopian capability of the FDIC makes there seem like there are no bad Banks.

The above screen-print was taken from the 2008 FDIC Annual Report. Good Lord, are they seriously bragging about having “Zero Insured Deposit Dollars Lost”? They have access to practically unlimited funds (think TARP 2008) of the Federal government and they want to brag about covering over the failures of bad Banks?

And that raises another point, something was indeed lost; the taxpayers fund and cover what the FDIC pays out; either with current tax money or when the Treasury bonds to cover deficit spending are paid with future tax money. Taxes are a loss to private citizens.

Let us chase the rabbit, a person pays taxes, a person opens a Bank account and deposits their money, the Bank fails, the FDIC covers the Bank failure paying Bank Customers with money the Federal government got from the Bank Customers via taxes in the first place. What a racket?

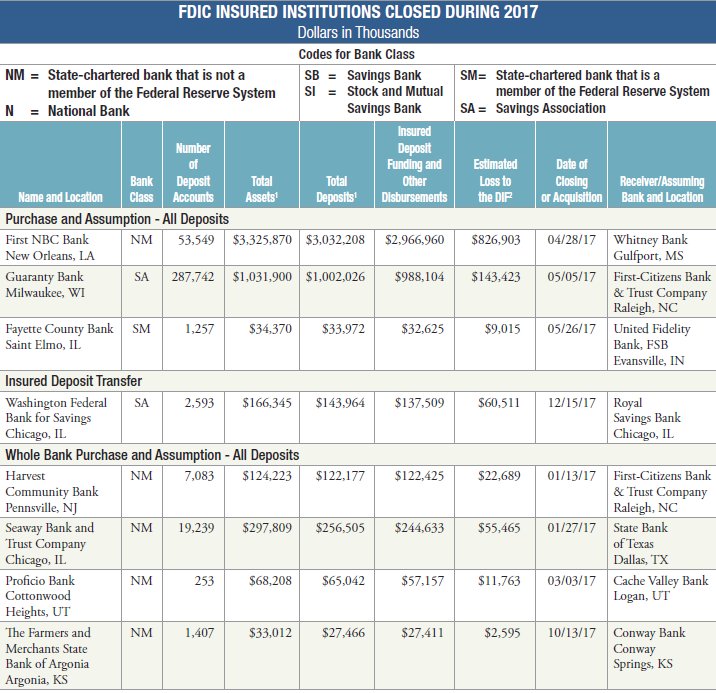

Concerning Bad Banks and their failures, how many times have you seen a Bank outright shut down and close their doors? Not very often. What is more commonly seen are Banks changing names. I know my presumption has always been, upon a Bank changing names, was that the Bank was purchased by another Bank. The above graphic taken from the 2017 FDIC Annual Report shows that when Banks fail, the FDIC covers the short-comings on Deposits, and then another Bank takes over via “Receivership”. That failure of the “Guaranty Bank Milwaukee WI” with 287,742 deposit accounts looks like it turned out to be a big bad Bank; but I forgot myself, with the FDIC there is no such thing as badness especially when the taxpayer will chip in.

Concerning Bad Banks and their failures, how many times have you seen a Bank outright shut down and close their doors? Not very often. What is more commonly seen are Banks changing names. I know my presumption has always been, upon a Bank changing names, was that the Bank was purchased by another Bank. The above graphic taken from the 2017 FDIC Annual Report shows that when Banks fail, the FDIC covers the short-comings on Deposits, and then another Bank takes over via “Receivership”. That failure of the “Guaranty Bank Milwaukee WI” with 287,742 deposit accounts looks like it turned out to be a big bad Bank; but I forgot myself, with the FDIC there is no such thing as badness especially when the taxpayer will chip in.

Another facet, how many people engaged in authoritarianism, vice and sin profit from the behavior of these bad Banks? And then get away scot free with their ill-gotten gains when the Bank fails? Right in front of our faces? And remember, a person making $100,000(+) a year anywhere in this process, let alone bonuses, without any other profit…once the Bank fails…that yearly wage was an ill-gotten gain.

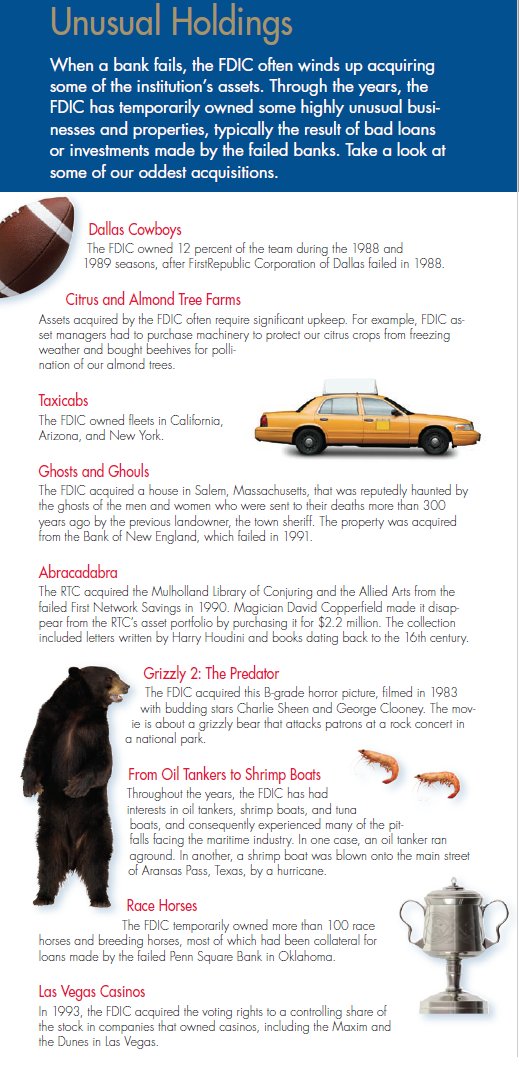

What happens when a Bank fails and there is no other Bank to step in immediately for “Receivership”? The FDIC takes possession of the Bank and its assets until it can liquidate them. The below is a very interesting and disturbing graphic taken from the 2008 FDIC Annual Report.

So, the FDIC and by association the Federal Government has been involved in ownership, full or partial, for a period, of a professional football team, farms, taxicabs, movies, boats, race horses, and casinos.

So, the FDIC and by association the Federal Government has been involved in ownership, full or partial, for a period, of a professional football team, farms, taxicabs, movies, boats, race horses, and casinos.

What are the implications upon private property with this aspect of the FDIC? Are we witless to the fact monetary policy can be tweaked to drive Banks to failure allowing the FDIC and the Federal government to acquire private property in all its forms? What if the Federal Reserve constricts the money supply; how much and of what exactly will the FDIC come into possession?

Consider this post on CNBC.com on 03/08/2018:

JP Morgan co-president warns of ‘deep correction’ for stocks totaling as much as 40% over next few years.

“The equity market has some way to go for the next year to two,” said J.P. Morgan’s Daniel Pinto. “But then, if there is a correction, it could be a deep correction.”

How many Banks are going to fail “over the next few years“? How many “unusual holdings” will the FDIC pick up?

As of September 30, 2017, the number of insured institutions on the FDIC’s “problem list” (institutions with the highest risk ratings) totaled 104, which represented a decrease of more than 88 percent from December 2010, the peak year for bank failures during the financial crisis.

What spin! To try and make 104 Banks on the “problem list” look prudent by saying that number is 88% less than the peak year of bank failures in 2010. I feel warm and fuzzy knowing that statistic.

The below cartoon was published in the FDIC’s 2008 Annual Report.

Only the credulous would not ask, “What Bank?” A private bank? If so, aren’t they capable of protecting their customer’s money without the government intervening?

Insurance is the antonym of gambling. By implication, if a Bank needs insurance, whether privately or the governmental FDIC, it is doing something risky. A definition of gambling is to put money at risk. A definition of insurance is to mitigate risk. If you deposit your money in a Bank that needs insurance you should pay attention to the terms under which that Bank operates.

“As of September 30, 2017, the FDIC insured $7.1 trillion of deposits at 5,746 commercial banks and thrifts,…”

And none of that would be necessary if good Banks were patronized and bad Banks faced criminal charges upon failure exponentiated by the number of customers they defrauded or stole from.

Please support our coverage of your rights. Donate here: Paypal.me/RedoubtNews